Practical Guide to Bank Branch Audit 2026 (E-Book) available at ₹499 – Limited Time Offer - Click Now

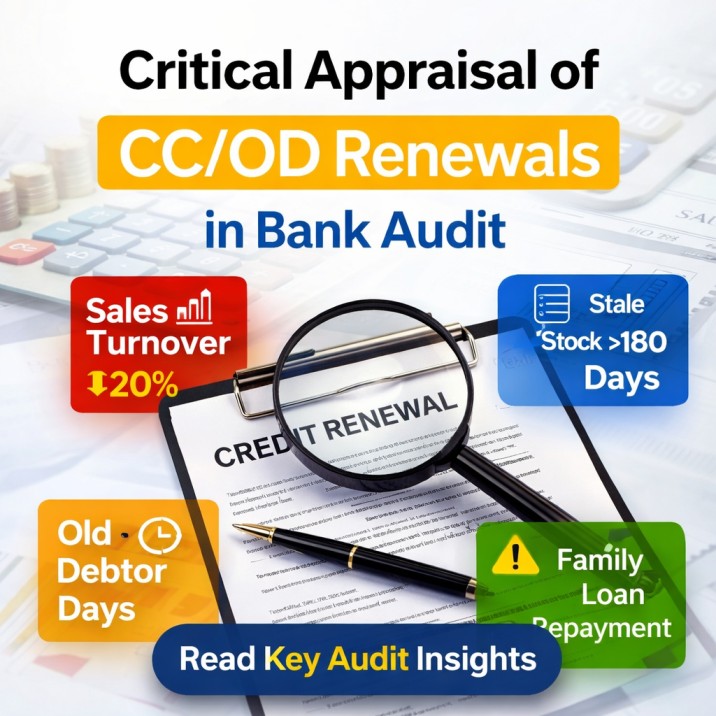

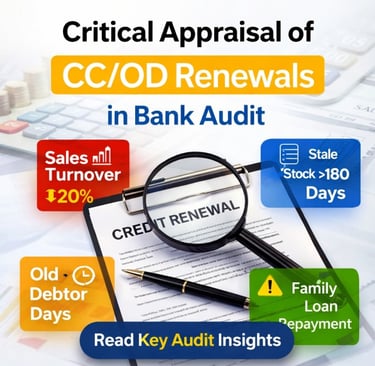

Critical Appraisal of CC/OD Renewals in Bank Audit: A Practical Guide

LOAN & ADVANCES BLOGS

CA Parikshit Bhadade

3/5/20261 min read

CA Parikshit Bhadade

Expert Guidance in Bank Branch Audits, LFAR, NPA Compliance's & RERA Advisory.

Contact

Our Group website

caparikshitbhadade@gmail.com

+91 9105 569 555

© 2024. All rights reserved.